A world of trouble

Insured losses from strikes, riots and civil commotion in certain hot spot territories now comparable to major natural disasters

Howden highlights significantly reduced risk appetite in the political violence (PV) insurance market caused by an increasingly unpredictable threat landscape

- Recent unrest in South Africa and Latin America has seen the value of strikes, riots and civil commotion (SRCC) claims rival or even surpass major natural catastrophe losses

- The PV loss profile has shifted significantly in recent years, with (re)insurers suffering more than USD 10 billion of SRCC losses since 2015 vs less than USD 1 billion for terrorism

- Growing discontent across the globe has sent SRCC costs spiralling to the point where they can impede economic growth or even trigger recessions

- The Ukraine war has also exposed considerable geopolitical risks: the conflict is set to become one of the biggest PV losses on record

- Standalone PV pricing is undergoing a correction as a result, rising by more than 80% since 2018

11 April 2023, London – Underlying grievances tied to inequality, the cost of living crisis and broader disenfranchisement, combined with the lasting economic effects of COVID-19 and Russia’s invasion of Ukraine, have elevated SRCC risks in both advanced and emerging economies and caused a historic reset in the standalone PV market, according to a new report released by Howden.

Recent outbreaks of violence in Chile, the United States, South Africa and Peru reflect a highly dynamic and interconnected risk landscape. These events saw violence spiral quickly to affect multiple locations and are indicative of rising discontent globally, as demonstrated by other incidents of unrest last year in Iran, Kazakhstan, Sri Lanka and Argentina. 2023 has offered little respite, with protests in France and Israel hitting the headlines in recent weeks.

All of which has reset insurers’ views of risk. Property insurers are increasingly withdrawing SRCC cover whilst risk appetite in the standalone market has reduced significantly. The fallout represents something akin to a perfect storm – demand up, supply down, triple-digit loss ratios and reinsurance retrenchment – resulting in a market-changing pricing correction.

Market pressures have been compounded further by the war in Ukraine, which in addition to causing one of the largest PV losses ever, has also exacerbated cost of living pressures and exposed other geopolitical risks that currently extend to rising tensions between China and the United States.

Conditions have unquestionably become more difficult, but few areas of (re)insurance have such an innate ability to respond to a rapidly changing threat landscape. The step-change in losses and demand will require the market to scale up considerably over the next few years: Howden is leading the charge by leveraging expertise within our group and engaging with an array of market participants to entice more capacity into the market and secure the best outcomes for clients.

Structural change to the SRCC loss environment

The shift in loss profile has been stark. Whereas major PV market-related losses were confined mostly to large-scale terrorist bomb attacks previously, multi-billion dollar SRCC events in Chile (2019), the United States (2020) and South Africa (2021) have led to considerable payouts for insurers and reinsurers.

Increased frequency of severity has propelled the quantum of SRCC claims in South Africa and Latin America to rival or even surpass natural catastrophe losses (see Figure 1 for data since 2015). This is not down to a lull in catastrophe activity – both territories experienced a number of sizeable natural disaster losses during this time (including record-breaking floods in South Africa) – but a reflection of the unprecedented scale of civil unrest.

Figure 1: Natural catastrophe insured losses vs SRCC insured losses – 2015 to 20221 (Source: NOVA)

Tom Bradbrook, Executive Director, Howden Specialty, commented: “Such devastating losses have precipitated a correction in the PV market that looks set to persist for some time to come. Clients can therefore expect to continue to encounter difficult market conditions in 2023. For the cover that is most sought after currently – namely SRCC and full PV – line sizes are being cut across the board and certain risks are difficult to place, especially in more volatile areas. Rates are up for all perils and territories, with our pricing index showing an average increase of 80% since 2018.

“Now more than ever, risk transfer advice can make a crucial difference to renewal outcomes. With little prospect of a let up in market conditions, sector expertise, market-leading thought leadership and unrivalled relationships with insurers have never been more important. Howden’s PV team provides all this and more and we look forward to supporting clients in managing change and securing the best coverage available in the marketplace.”

Effects of Ukraine war

As well as being another billion dollar plus event – current estimates suggest the war in Ukraine will become the biggest PV loss since the standalone market was born 20 plus years ago – the crisis has aggravated an already hostile SRCC backdrop.

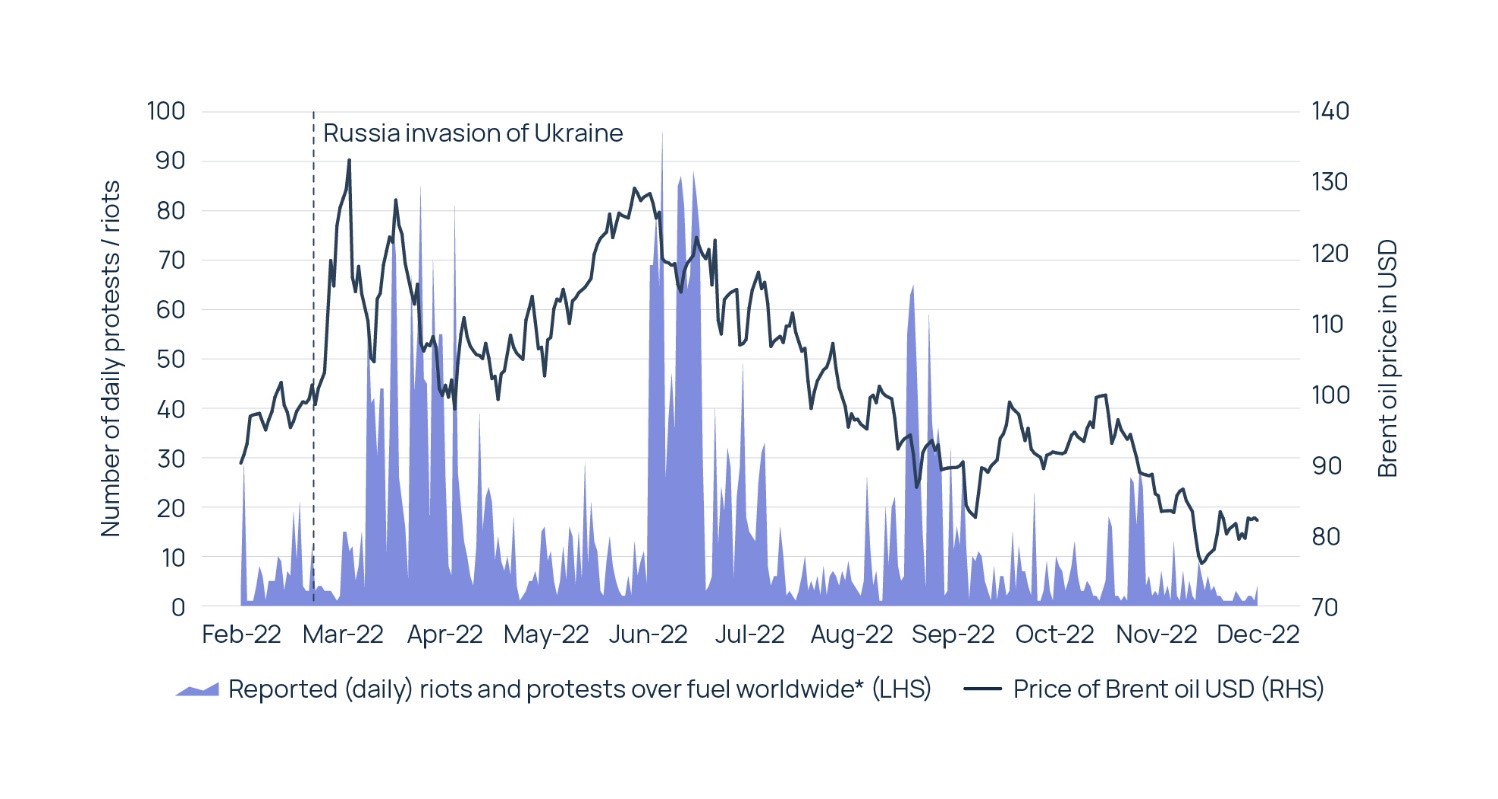

Whilst the causes of civil unrest are disparate and complex, and often tied to discrete national circumstances, sudden political and economic shocks, especially those that influence the cost of essential goods and services, can inflame grievances and lead to spontaneous protests. Figure 2 shows the correlation between the daily number of protests and riots worldwide linked to rising fuel prices and oil price fluctuations following Russia’s invasion of Ukraine in February last year.

Figure 2: Daily reported protests and riots over fuel prices vs cost of oil in 2022 (Source: Howden analysis using ACLED data, St. Louis Fed)

Transformational change to PV market

This highly dynamic threat landscape has brought about the most significant recalibration to the PV market since its inception. Following a period of high profitability for the best part of two decades, 2019 proved to be a watershed moment. Long-standing soft conditions, characterised by marked declines in pricing and strong competition, have been arrested by the series of losses that moved the overall market into the uncharted territory of underwriting losses.

Such a pronounced change has transformed the pricing environment. After a prolonged period of sizeable rate reductions through most of the 2010s, pricing stabilised towards the end of the decade before the correction started to materialise in late 2020, accelerating rapidly into hard pricing territory in 2022.

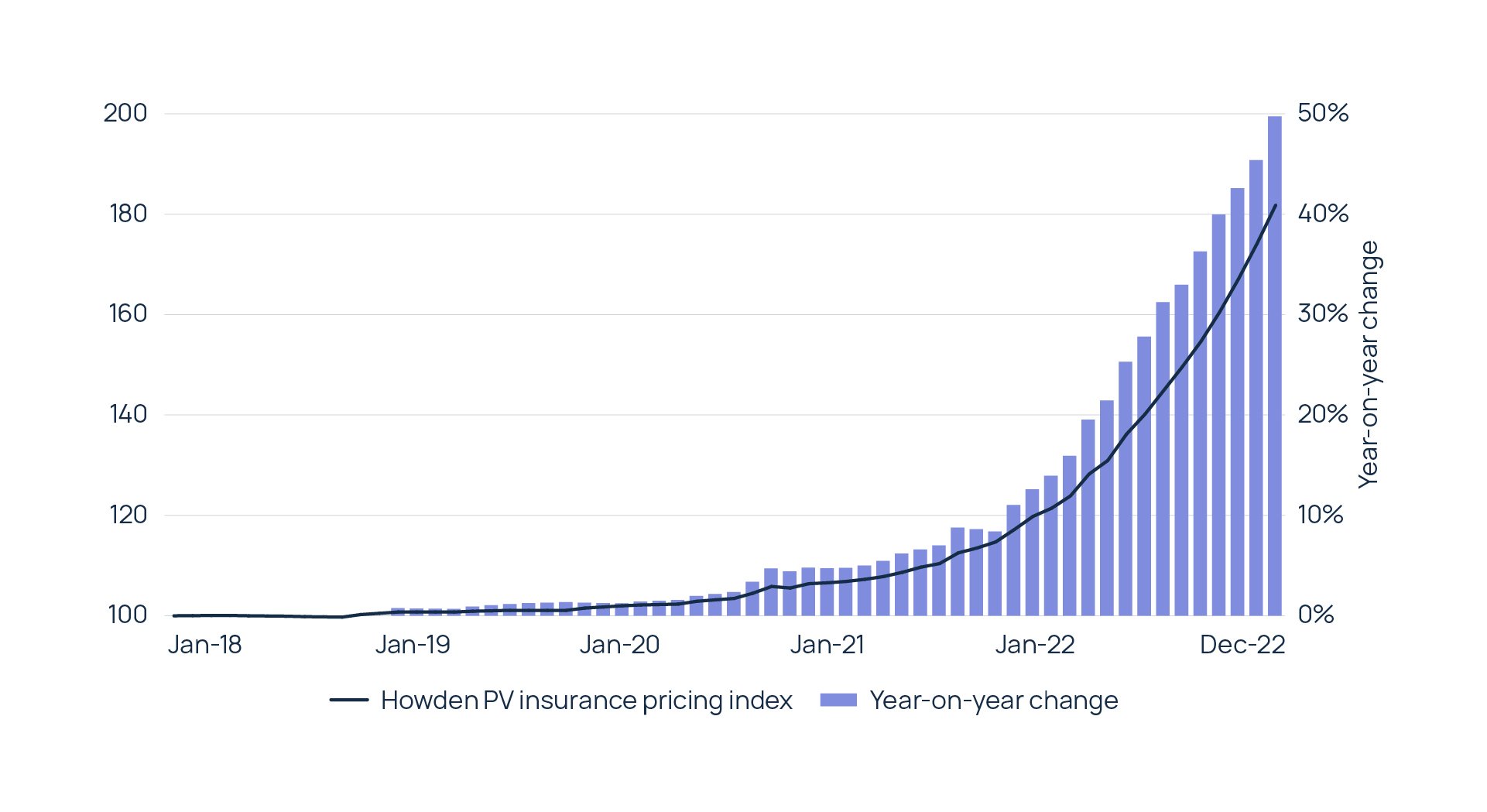

The degree of repricing is captured by Figure 3, which shows Howden’s Global Political Violence Pricing Index, along with average year-on-year rate movements, dating back to 2018. Pricing today is up more than 80% from its nadir in 2018.

Figure 3: Howden’s Global Political Violence Pricing Index from 2018 (Source: Howden)

Reinsurance market hardening

The correction in the PV market is likely to continue for much of this year, with pressures compounded by considerable tightening in the reinsurance sector during 1 January 2023 renewals. Retentions and pricing doubled in certain instances and considerable reinsurance protection was lost overall.

Steve Bessant, Executive Director, Howden Tiger, commented: “Treaty reinsurance appetite in this class declined at 1 January 2023, particularly for upfront carriers unwilling or unable to meet future treaty pricing expectations. The change was driven by the five key treaty reinsurers who, after recently sustaining disproportionately large losses from both standalone and all-risk policies, refused to continue on previous unprofitable conditions.

“The effect of this change varied by peril, with capacity commitments reducing for SRCC and full PV by as much as 30% and 60%, respectively, and pricing increasing significantly across the board. Event definitions and terms and conditions likewise tightened at 1 January 2023, as treaty reinsurers reduced exposures, particularly in the contingent business interruption space. These dramatic changes have cascaded down the value chain, forcing original insurers to pass on restricted wordings, higher costs and deductibles to buyers.”

Read the full report